Can better pre-trade data really unlock liquidity in frozen fixed income markets?

If buy and sell-side bond traders are to see real benefits from the pre-trade data they receive, it has to increase the efficiency of their trading. To do that, it not only needs to represent a realistic picture of the market, it has to do so reliably as market circumstances change.

Data consumers in the bond market are not fully satisfied with the level of transparency they have into the market. The differences between what they need and what they can access, stems from challenges in the existing supply of data sets, which need to be improved upon, but also in data which is currently inaccessible. Bridging these gaps can potentially reduce information leakage and increase market making activity.

For data providers tackling the first challenge, traders need to know that what they see is data that accurately represents market activity.

“The universal theme that we hear from the buy side, is regarding pricing information that they’re seeing from dealers – what does it actually reflect?” says Chris White, CEO of BondCliQ, a post-trade pricing data aggregator. “When the International Capital Markets Association (ICMA) set out different classifications for quotes, that illustrated a larger problem, which is, how do buy-side clients differentiate the reliability of pricing information? What is actionable and reliable, for trading and evaluation? Our theory is that the reliability of the pricing information is directly related to the confidence of the price provider. Confidence on the dealer side can only be improved if they themselves have greater access to data, because then they can know whether or not their price is an accurate representation of their intention.”

These efforts to improve the accuracy of data have required input from both sides of the street and market data providers.

“There has been a lot of discussion in the industry around pre-trade axes and defining the terminology around pre-trade information,” says Gareth Coltman, global head of trading automation at MarketAxess. “We were involved with ICMA looking at defining these terms, what they mean and what clients would like to see. I think that has increased quality and accuracy of pre-trade data. We’re working with our dealer clients, to integrate that terminology into the system to take the axes from what historically was relatively low speeds of update, to something more like a real time streaming indication. We’re closing that gap. And that’s true, globally, in Europe probably more so in the US.”

Getting to grips with data

To understand how existing data can be improved, it is worth reviewing what it currently available. Data used pre-trade, to assess how and with whom to trade, is typically provided by both independent vendors and trading venues. It can either be provided as raw information which needs to be cleaned, filtered and consolidated, or as a more complete product.

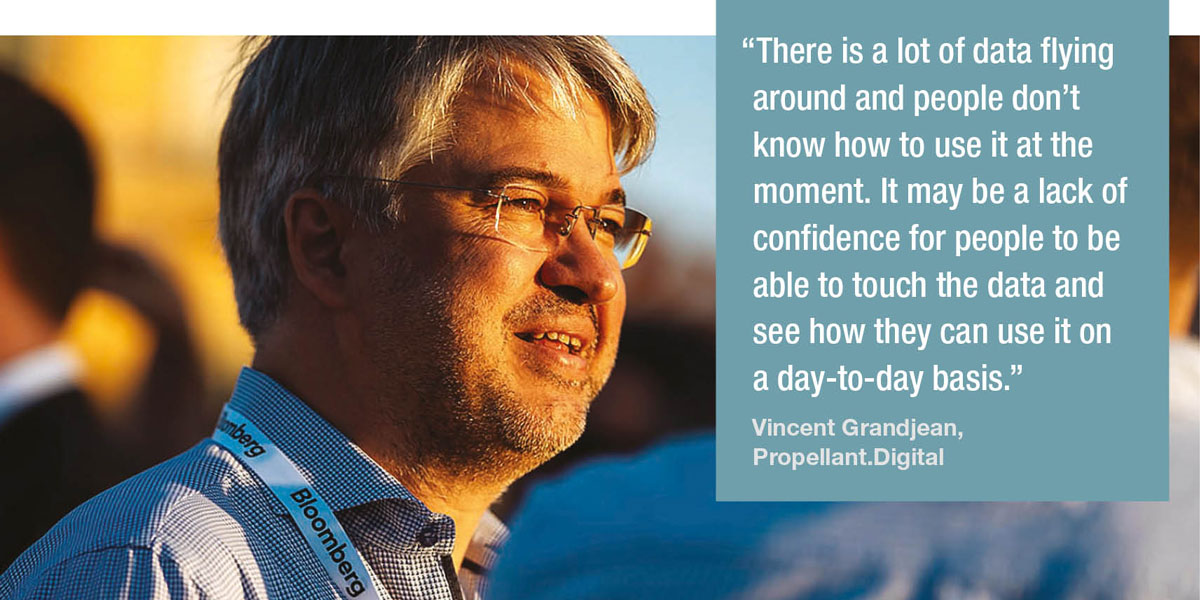

“The value is in how they use data in their trading workflow,” says Vincent Grandjean, CEO of Propellant.Digital. “There is a lot of data flying around and people don’t know how to use it at the moment. It may be a lack of confidence for people to be able to touch the data and see how they can use it on a day-to-day basis.”

In the US a post-trade tape – TRACE – has existed since 2006, while in the European Union and the UK such consolidated tapes of trading activity are still in the planning stages. Knowing what is available – and how it can be used – can be the biggest initial gain that a firm can make in order to improve pre-trade analysis.

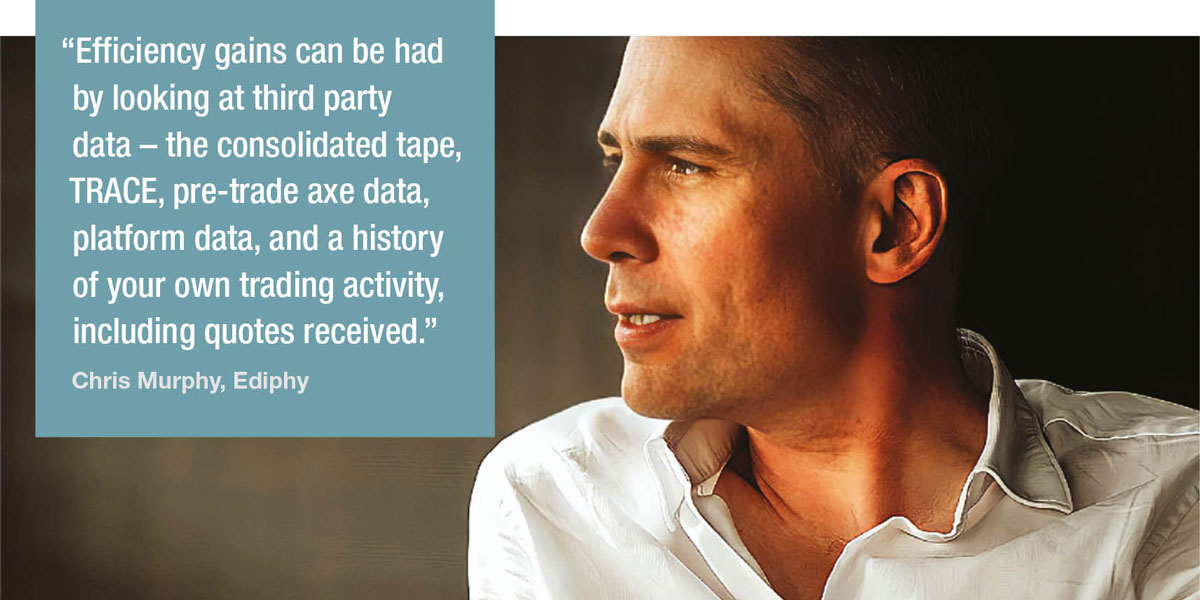

Chris Murphy, CEO of Ediphy, says, “Efficiency gains can be had by looking at third party data – the consolidated tape, TRACE, pre-trade axe data, platform data, and a history of your own trading activity, including quotes received.” He adds, “You need to know who was competitive and who wasn’t. That is going to make it more efficient for you to manage instrument selection in a portfolio and how to trade that instrument in the most effective way.”

For firms that have awareness of the available data, they must also have the skill and tools to enable them to arrange that into a picture which is useful.

“Decision making and execution optimisation is still just scratching the surface,” says Gio Accurso, MarketAxess. “With better, more accurate pre-trade tools, with the emergence of new trading protocols, we are starting to see data guiding clients in how to trade. The issue is less about where data is going and more about how different data is evolving.”

Murphy says, “We’ve been thinking about a dashboard which is context specific to an order, position or a particular item that a portfolio manager might want to put in their portfolio. Does it have the right yield and risk dynamics to fit within my portfolio but also, what’s the likelihood of me being able to trade this anywhere near the mark on the screen?”

New data ideas

Overcoming the second challenge relies on greater innovation – and potentially new sources of information that can represent trading dynamics which are currently concealed, allowing firms to manage risk more effectively.

“There are initiatives out there to create more evaluated pricing, inferring where things might trade based on where it traded most recently and also information sharing networks,” says Murphy. “All of them can add value to the process. But we think the biggest gap is in the tools to harness this data.”

Tension around the capabilities of data to support activity has been worsened as sell-side market makers have taken a step back during stressed market conditions, for example in the recent UK gilt market sell-off.

“We never got any criticism [of pricing data] during the gilt market sell-off, and generally a lot of our models are valued and seen as important because they do give the users the chance to react to events,” says Accurso. “Bear in mind the difference between a model predicting the future and our models. When we are providing real-time pricing tools, whether CP+ or a relative liquidity score, those are less affected by volatility because they use intraday features and information, so they hold up pretty well. They predict what is happening in the market now, not in two hours.”

One of the biggest market structural differences between the equity market and the fixed income space is the lack of a primary exchange which lists securities in fixed income. In the stock market this creates a centralised point of liquidity and price formation.

Finding an alternative way of assessing liquidity in bond markets would create considerable value for traders, potentially reducing the risk in taking positions.

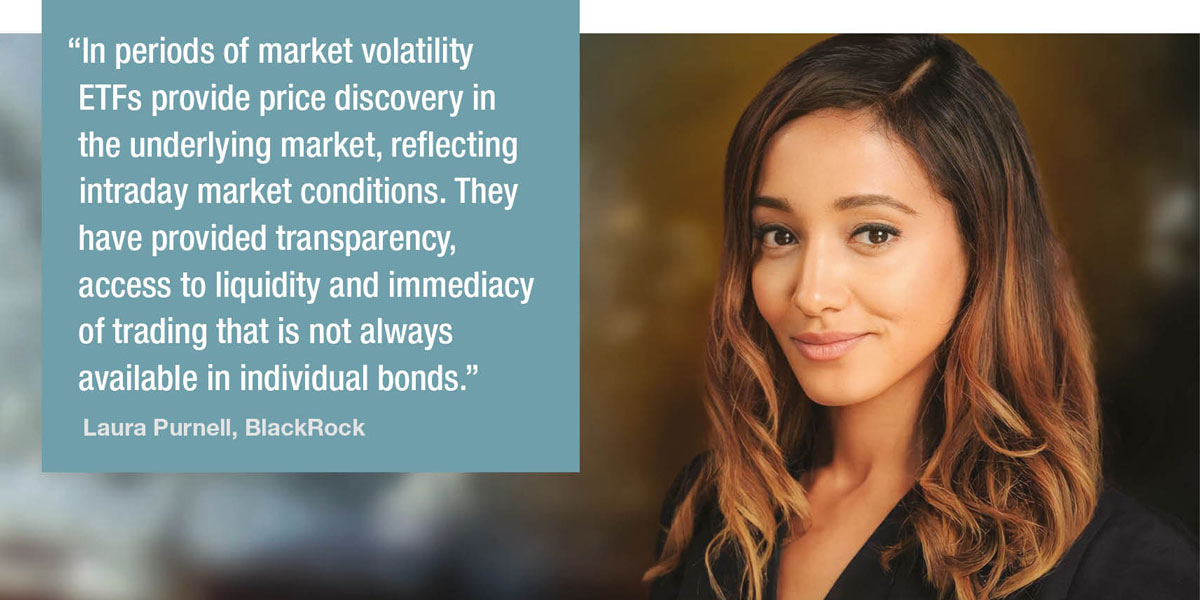

“Although only a fraction of the total fixed income market, exchange traded funds (ETFs) are increasingly providing valuable trading data,” says Laura Purnell, director and fixed income trader at BlackRock. “In periods of market volatility ETFs provide price discovery in the underlying market, reflecting intraday market conditions. They have provided transparency, access to liquidity and immediacy of trading that is not always available in individual bonds. As a result, investors have increasingly turned to ETFs to allocate capital, adjust positions and manage risk.”

The information of which securities are held by which firms is contained within central securities depositories (CSDs) and this has been considered a viable source of new data – notably in an effort by pre-trade data provider Algomi, now known as Lucera LumeAlfa.

“Holdings data within CSDs could be extremely valuable to the market,” says White. “The diversity of holders, and the type of holders, have a direct and meaningful impact on the secondary liquidity of a given bond. For example, if an issue with a billion dollar float is 65% held by insurance companies, then the true float is much smaller than the outstanding notional. Operating in the current market without the objective holdings data is hazardous, because you need more information on the market making side or the buy side to make an informed decision about the secondary trading characteristics of the bond.”

©Markets Media Europe 2025