In its latest ‘Europe Credit Markets Update’, S&P Global Ratings has painted a grim picture for European borrowers, notably in the high yield space, which it labels ‘speculative grade’.

Although it found that overall negative rating activity has reduced from Q1 and spreads have tightened since the March volatility, defaults this year have already overtaken the previous four years’ count. It found that spreads for European speculative-grade issuers had increased, as a result of concerns around COVID-19, oil and the subsequent economic impacts.

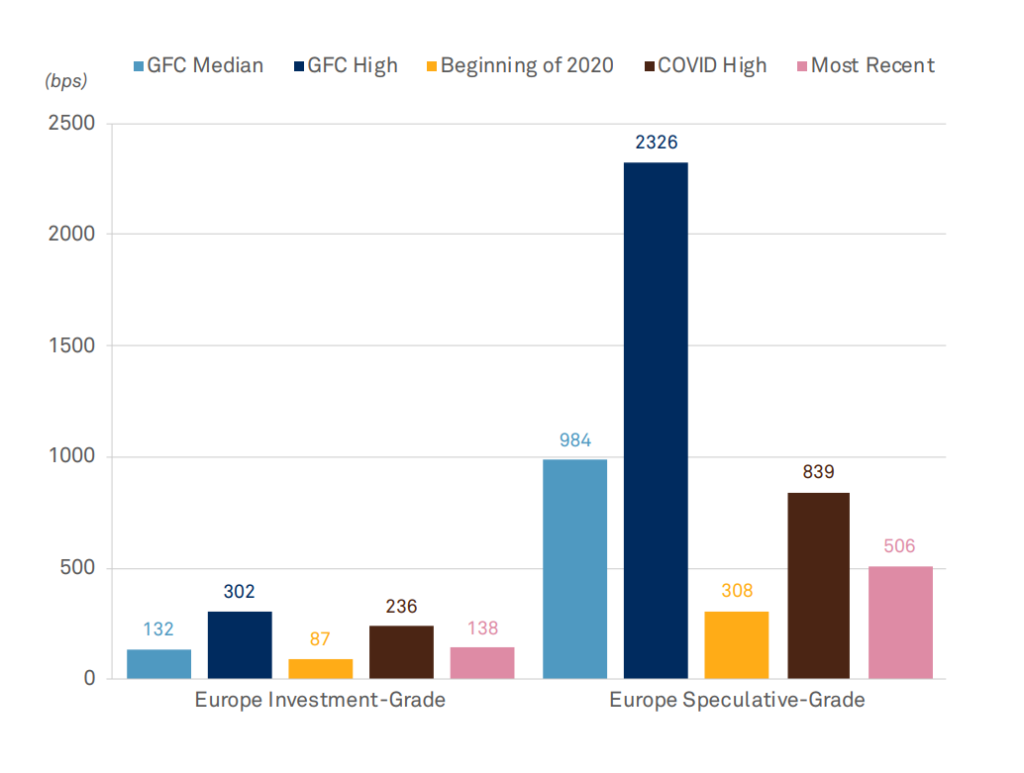

“At this year’s high, European spec-grade spreads were nearly three times— around 530 basis points (bps) above the level at the beginning of the year,” it wrote. “Nevertheless, the recent peak in spreads was less than 40% of what was seen during the GFC. More timely and stronger monetary and fiscal responses, notably the ECB’s €1.3 trillion pandemic emergency purchase programme (PEPP) reassured investors and calmed markets. Consequently, spreads for speculative-grade decreased more than 320 bps by mid-June.”

Investment grade spreads at 138 bps were still higher than at teh start of 2020 and also slightly higher than the median of the global financial crisis (GFC) of 2008.

According to S&P Global Rating’s research, approximately 47% of speculative-grade issuers are exposed to downgrade risks and 56% of the risky borrowers are vulnerable to credit deterioration. In the most risky credit categories – B- and lower – banks, consumer products, leisure, hotels/bookings, and entertainment businesses have the highest count of negative outlooks and placements on ‘CreditWatch Negative’. CreditWatch is labels the potential direction of a short- or long-term rating, and ratings can be placed on CreditWatch when an event or a deviation from an expected trend occurs.

Under its rating system ‘Weakest Links’ are issuers rated ‘B-’ and below with a negative outlook or on CreditWatch with negative implications. According to S&P Global Ratings they usually have a default rate that is eight times that of speculative-grade issuers. In Q2 it found that Europe has seen weakest links rise to 99 issuers, making up nearly 19% of the speculative-grade rated group.

As European banks are indirectly exposed to the COVID-19 impact they have a ‘significant negative bias’ but no bank debt issuers are rated as CreditWatch negative, which means there is a lower immediate potential for them to be downgraded. Sectors most at risk of downgrade potential are automotive, media and entertainment, and transportation which have been the hardest hit in Europe.

While issuance of investment-grade bonds has overtaken April 2019 levels with a notable surge following the European Central Bank’s announcement of bond purchasing programme on 18 March, speculative-grade issuance is slightly below the level seen in 2019.

©Markets Media Europe 2025