The DESK’s research supported by LTX, finds liquidity improving, larger electronic trade sizes and greater use of data science pre-trade.

The DESK’s research supported by LTX, finds liquidity improving, larger electronic trade sizes and greater use of data science pre-trade.

In 2024 bond markets are seeing an improvement in the supply of liquidity and narrower bid-ask spreads. Nevertheless, to take advantage of this, buy-side traders need to navigate a bond market that is growing in size through record debt issuance, whilst facing pressure to process the primary market activity and add value to secondary market trading.

As liquidity in debt markets is episodic, the overall improvement of liquidity conditions masks the complexity buy-side traders face. They need to execute trades in the most efficient way possible to minimise information leakage and maximise price and speed. Increasingly, some of the more efficient methods of execution for larger numbers of bonds are portfolio and list trading.

There is so much potential information available to identify a counterparty, it becomes ‘noise’ for a human trader if it is not filtered effectively, using data science techniques, quantitative analysis and artificial intelligence patterning to pick out the useful and viable information for a given trade.

In 2022, The DESK analysed liquidity access and data science usage for mid-sized asset managers in the US market. Mid-sized firms were focused on for the purpose of eliminating distortions in the data created by very outsized order flows from buy-side firms with over US$1 trillion in assets under management, and those smaller firms whose order flows penalised them for limited trading activity. The research found that, at that point, liquidity support was worsening and the use of data science was nascent.

In 2024 we looked at the issue again via a similar piece of research in order to assess the state of the market. We found things had changed dramatically – and positively.

Executive summary

This report looks at liquidity access and execution dynamics in US fixed income markets, through the lens of availability and pre-trade transparency of that liquidity.

Our research seeks to minimise any bar-belling of results, by reporting on feedback from 33 mid-tier asset managers in the US fixed income market.

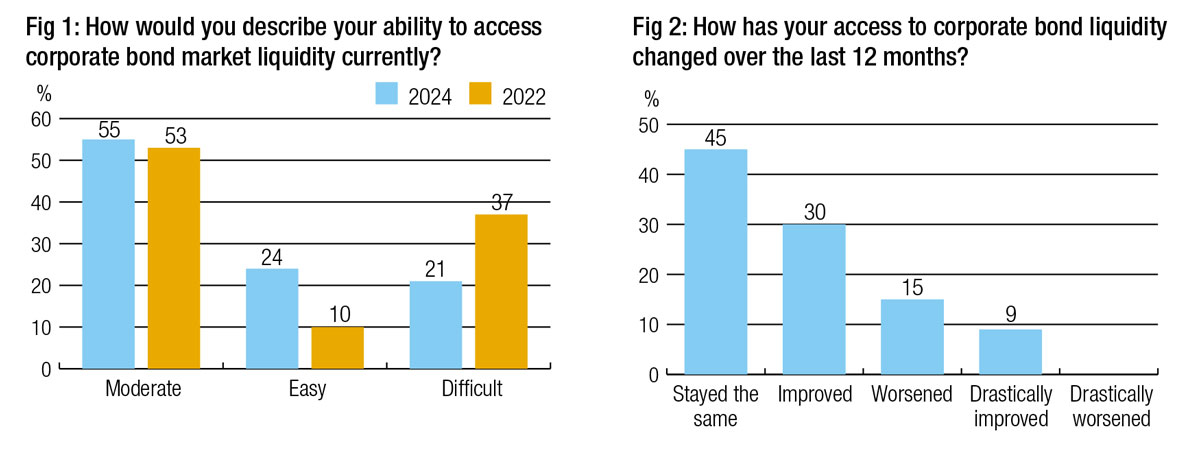

In 2024, liquidity access for mid-sized asset managers is improving for many (Fig 1), and worsening only for a minority. Finding a counterparty to trade at size is the most challenging execution objective.

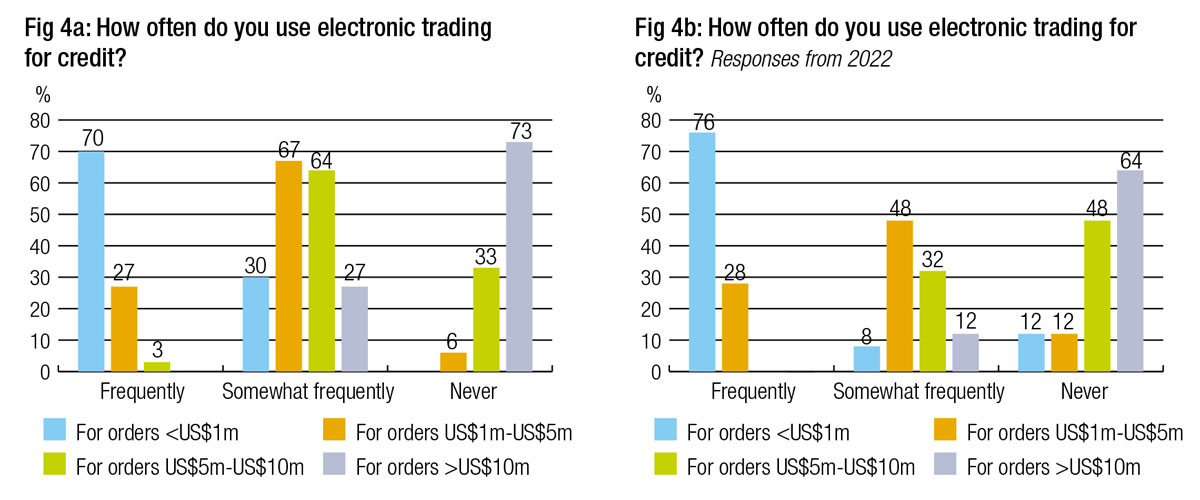

Consequently, getting better access to large in size trades would be a key motivator to trading electronically, followed by even better pricing. Electronic trading is still geared towards smaller-sized trades (Fig 4a), with the majority of respondents never using e-trading for large in size trades.

We see that a greater proportion of traders are now using electronic trading for larger orders than were in 2022, while the number who ‘never’ use e-trading for trades of all sizes has declined (Fig 4a & 4b).

The application of data science in counterparty selection is used by the majority of firms (Fig 6) to at least some degree – it is accessible in most trading platforms today, and the shift from post-trade to pre-trade transaction cost analysis (TCA) appears to be the driver for this change.

That represents a big shift from the report in 2022, although this could reflect more participation from systematic firms in the survey.

Artificial intelligence has become widely discussed in the market (Fig 7), although only a fifth of firms are using it to any extent as part of trading. Its development by trading platforms allows for its application deriving key insights from many large datasets and models, with human traders still calling the shots as to how the output is then used in executing trades.

Interestingly, over half of respondents predict that they will increase their use of AI in the future, reflecting the intention to test – if not adopt – these tools looking forwards.

Liquidity accessibility in 2024

Buy-side traders in 2024 have reported that access to liquidity has mostly been ‘Moderate’ (55%) to ‘Easy’ (24%) with just 21% indicating that access was ‘Difficult’. This reflects a significant improvement from the 2022 survey, when just 10% of respondents reported access was ‘Easy’ and over a third – 37% – reported it was ‘Difficult’ (Fig 1).

For traders, this also ties in with a couple of other trends. Bid-ask spreads have been tightening in US credit markets this year according to trading sources, while trade sizes in US investment grade are declining, according to Coalition Greenwich, which in 2023 found “more electronic trades over $2 million in size today than we ever have,” but added, “The biggest of institutional blocks ($5 million and up) continue to happen bilaterally.” That suggests we are seeing lower costs for accessing liquidity in US markets, which tallies with the survey’s analysis.

39% of respondents cited an improvement in liquidity access over the previous year (2023), which saw debt market challenges around the UBS / Credit Suisse merger and the US mid-sized bank crisis. Of the 39% who observed improved liquidity access, 9% reported that the improvement was drastic. Just 15% saw liquidity worsen relative to the previous year, and 45% reported it had stayed the same. No firms reported that liquidity had ‘drastically worsened’ (Fig 2).

As liquidity in fixed income is episodic and typically surges following the issuance of a new bond, the record levels of primary market issuance seen in Q1 2024 have undoubtedly played a role. Equally, the increased electronification of trading has likely reduced friction in finding and accessing liquidity.

Trading challenges

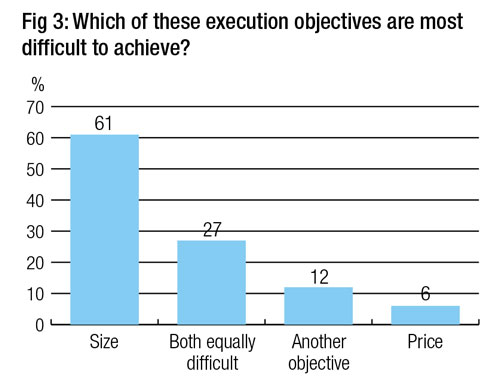

When asked about the greatest challenges in trading, 61% of respondents cited size as the hardest execution objective to achieve, with 27% reporting that both size and price were the hardest to realise. Other objectives – with citations including speed of execution and portfolio trading – were noted by 12% of traders, while 6% settled on price alone (Fig 3).

When asked about the greatest challenges in trading, 61% of respondents cited size as the hardest execution objective to achieve, with 27% reporting that both size and price were the hardest to realise. Other objectives – with citations including speed of execution and portfolio trading – were noted by 12% of traders, while 6% settled on price alone (Fig 3).

Given the tightening of bid-ask spreads in US credit markets this year, these results are not surprising, but it is good to note that mid-sized investment firms are seeing the impact of these reductions.

Investment banks typically vary pricing based on the profitability of the buy-side client, It may be that the typical mid-sized asset manager has a volume of orders which are not profitable enough to enable dealers to fully provide balance sheet to support liquidity. It is also worth noting that the demographic of mid-sized firms captures a number of systematic firms, whose order flow will be quite different to that of long-only active managers, who typically trade less frequently in larger size.

The split of e-trading for orders of different sizes is predictable – it is commonly used for smaller orders and rarely used for larger orders (Fig 4a).

Relative to 2022, the results show little change in the frequent use of e-trading, but considerably more comfort with trading ‘somewhat frequently’ for trades of all sizes (Fig 4a), which largely reflects a shift from the users who previously would ‘never’ use e-trading, notably for larger sizes. This suggests that block trading is increasingly moving from voice to electronic platforms.

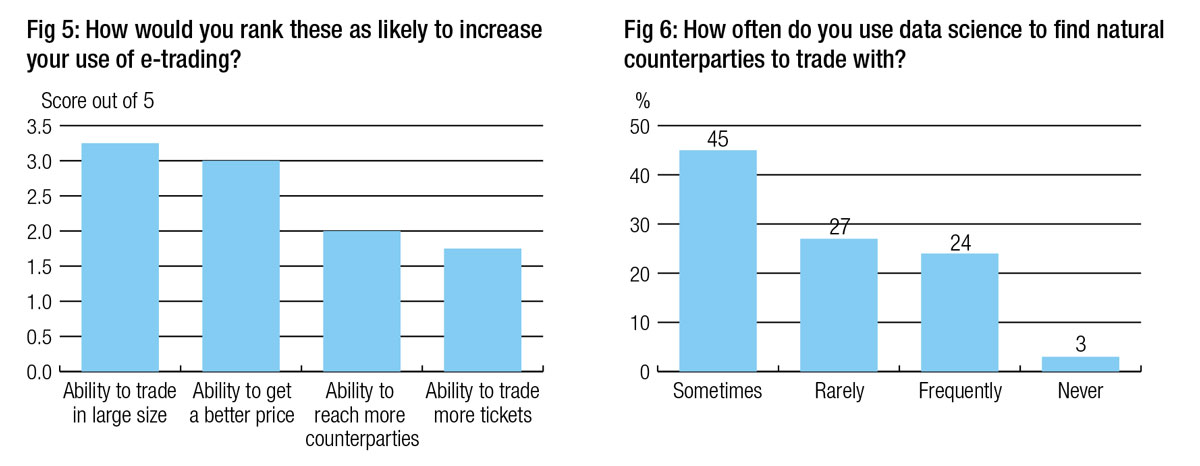

The value of electronic trading was perceived to be tied to the potential execution of larger sized orders, along with price, which it is already potentially compressing. When asked which improvements to execution objectives would likely increase the use of e-trading, currently 45% for IG and below 30% in HY according to analyst firm Coalition Greenwich, ‘Size’ was ranked most highly followed by ‘Price’, then the ability to reach more counterparties, and finally the ability to trade more tickets (Fig 5).

The science of trading

Over the past two years, the development of more sophisticated electronic trading protocols and pre-trade liquidity sources, notably those supported by trading venues, have enabled traders to optimise their access to liquidity directly within their trading workflows. For example, list trading, portfolio trading, and auto response capabilities represent different ways for buy-side desks to engage with the market, often based on different trading objectives.

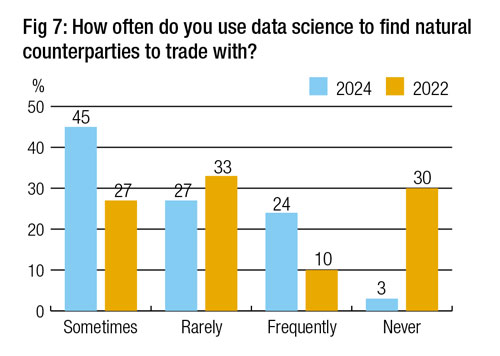

In 2024, almost half of buy-side traders say that they sometimes use data science to find a natural counterparty to trade with. Just under a quarter (24%) frequently use data science in this way. About a quarter (27%) rarely use data science in their counterparty selection, and 3% never use data science in this way (Fig 6).

Looking back, this is a considerable advance on the data from 2022, when 30% of traders never used data science to find a counterparty and 33% rarely used it.

The number of participants using data science in their counterparty selection frequently has more than doubled from 10% in 2022 to 24% in 2024 (Fig 7). This undoubtedly reflects both internal investment by asset managers in both data sources and tools, and the platform-led advances which help traders to find liquidity and counterparties on specific platforms.

The number of participants using data science in their counterparty selection frequently has more than doubled from 10% in 2022 to 24% in 2024 (Fig 7). This undoubtedly reflects both internal investment by asset managers in both data sources and tools, and the platform-led advances which help traders to find liquidity and counterparties on specific platforms.

This improvement to pre-trade transparency cannot help but boost overall access to liquidity, as is being reported by traders.

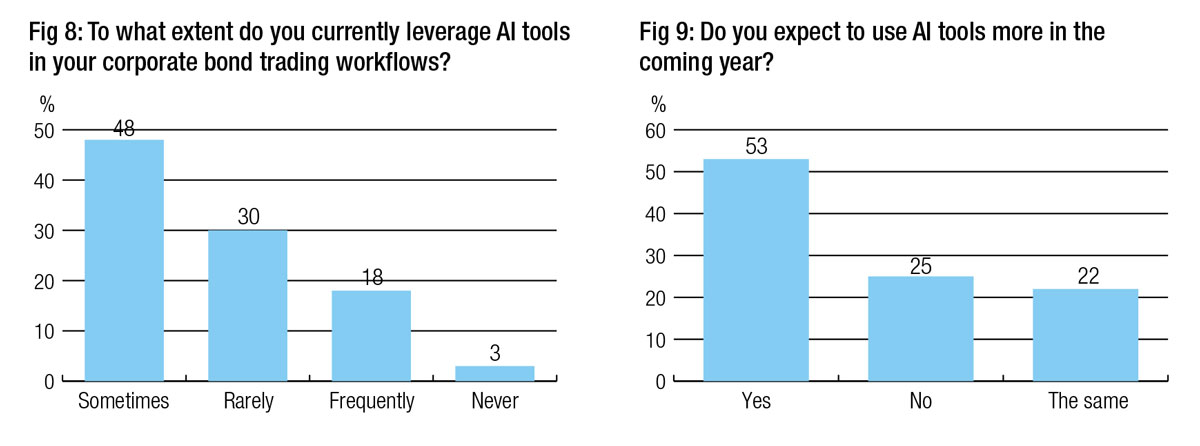

A more specific application of data science through the use of artificial intelligence tools is also observed, albeit at a lower level than data science more broadly. Currently 21% are using AI tools in their corporate bond trading workflows somewhat frequently or frequently (Fig 8).

While that means the majority are not using AI often, a fifth of traders are using AI frequently to some extent. That is considerably higher than would have been expected two years ago and clearly reflects the application of AI tools by trading platforms in both pre-trade and at trade analysis, along with post-trade transaction cost analysis, which can be fed back into pre-trade decisions. There is significant potential for growth in this space, with 78% of traders saying that they currently rarely or never use AI in their corporate bond trading workflows (Fig 8).

As the market more broadly becomes aware of the ways that AI and GenAI can bring benefits to their workflows, 21% have already operationalised and implemented these capabilities into their business processes (Fig 8). A larger majority have begun experimenting with these technologies and understanding their use cases and possibilities. Over half of respondents expect to increase their use of AI in the coming year (Fig 9).

Only one quarter does not expect to use AI tools more frequently in the next 12 months, and around the same amount of respondents don’t expect to change their current level of use (Fig 9).

Conclusion

The adoption of electronic trading, data science and ultimately artificial intelligence is closely correlated with improving liquidity condition for mid-sized buy-side firms. There are clearly environmental and structural reasons that can lead to improving liquidity in the corporate bond markets, and these should be considered collectively as potential drivers for the improvements.

Electronic trading is often a lower touch approach for traders, and that is geared towards lower risk, highly liquid smaller trades that can be easily prioritised based on price.

The challenge that still exists, even in a market with tighter spreads and higher liquidity levels, is trading in larger size without leaking information about a trade to the market. That requires advanced pre-trade understanding of which dealers to select and which bonds to source, in order to minimise time spent and noise generated around dealer selection.

The application of data science can deliver this, by providing traders with a clearer pre-trade picture of the market and outlining all of the choices available which will optimise each engagement. Electronic trading of blocks increases the efficiency of this order execution process and mitigates potential information leakage.

It is clear that many buy-side firms are on this path to better execution. It is also clear that the application of new technologies in this space is still relatively nascent, but is proving promising and continues to evolve at a very rapid rate.

Over the next twelve months it would seem likely that the delivery of electronic trading, supported by pre-trade AI and data science tools will mature, allowing firms that have already begun adopting and experimenting with this technology to achieve better access to large-in-size credit trading.

Not only does this match the needs of buy-side firms in managing costs and overheads for their trading functions, while delivering better execution results, it also tackles the elephant in the room; if and when liquidity conditions worsen, trading desks will need to find large blocks of liquidity at speed without relying on the manual process of telephones and IB chat, if they want to get ahead of the market.

©Markets Media Europe 2024

©Markets Media Europe 2025

story is AI")

more valuable")