Onboarding time shows the challenge facing EMS & OMS firms but algo trading increases demand

Two years ago Flextrade had a big pipeline of new business – only now does appear to be converting into users. The limited appetite for change exemplifies the struggle providers of execution and order management systems face, but also that this challenge can be overcome. Automation and algo trading is ascendant in the functionality demands from users.

OMS use

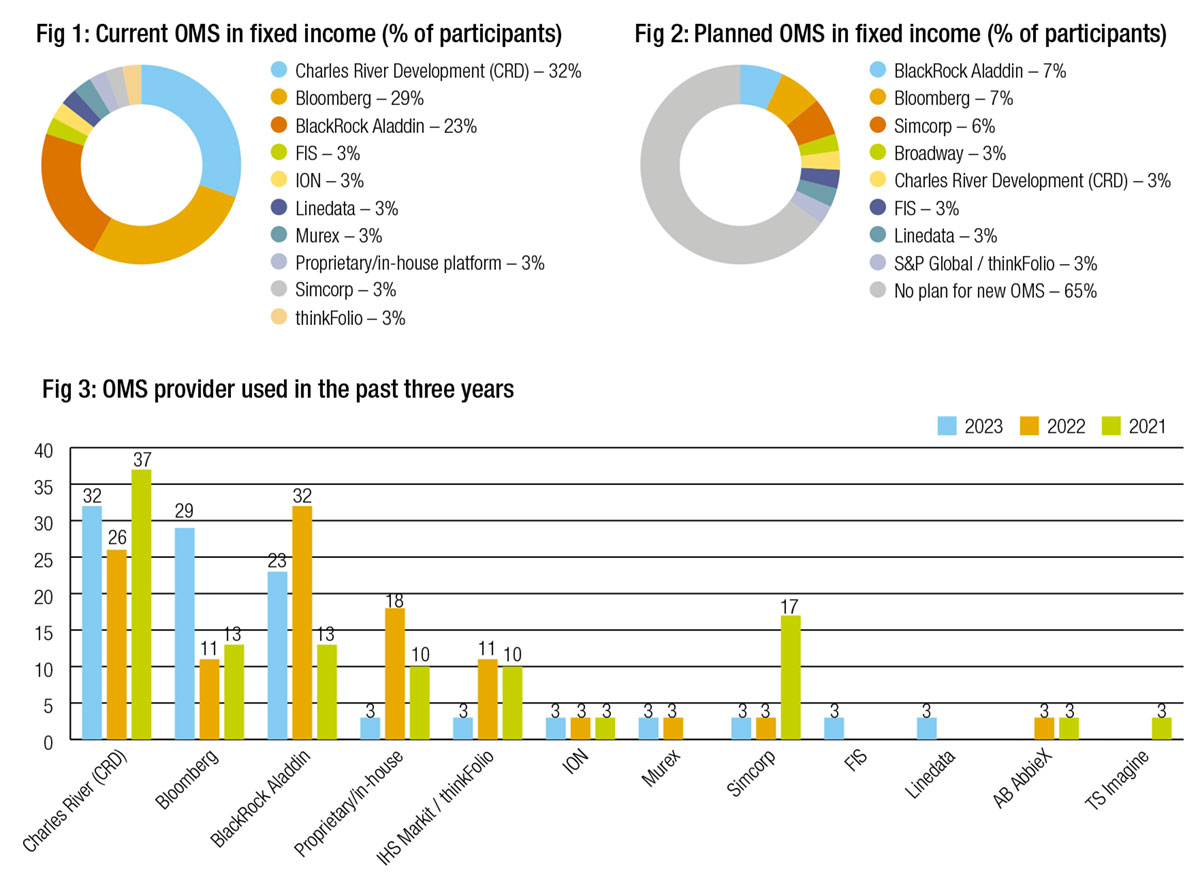

The latest survey into use of execution and order management systems by buy-side fixed income traders has shown a solid base for the major OMS providers, including Charles River, Bloomberg and BlackRock Aladdin, with few competitors emerging to threaten the big three (see Fig 1).

Interestingly this year we saw a significant decline in the use of proprietary desktop tools, despite concerns on both sides of the Atlantic that desktop technology might be regulated as a trading venue if it is a third party system that matches trading venues too closely.

Over the past three years we have seen little incursion by new players or even established challengers into the territory occupied by the top three, which is perhaps not surprising given the very limited deployment of new OMSs which occurs annually (see Fig 3).

If we look at the potential for new sales in the space it is clear that the tried and tested platforms are still favoured, with low levels of interest in new providers – the vast majority (65%) of respondents express no interest currently in switching to a new OMS (see Fig 2).

EMS use

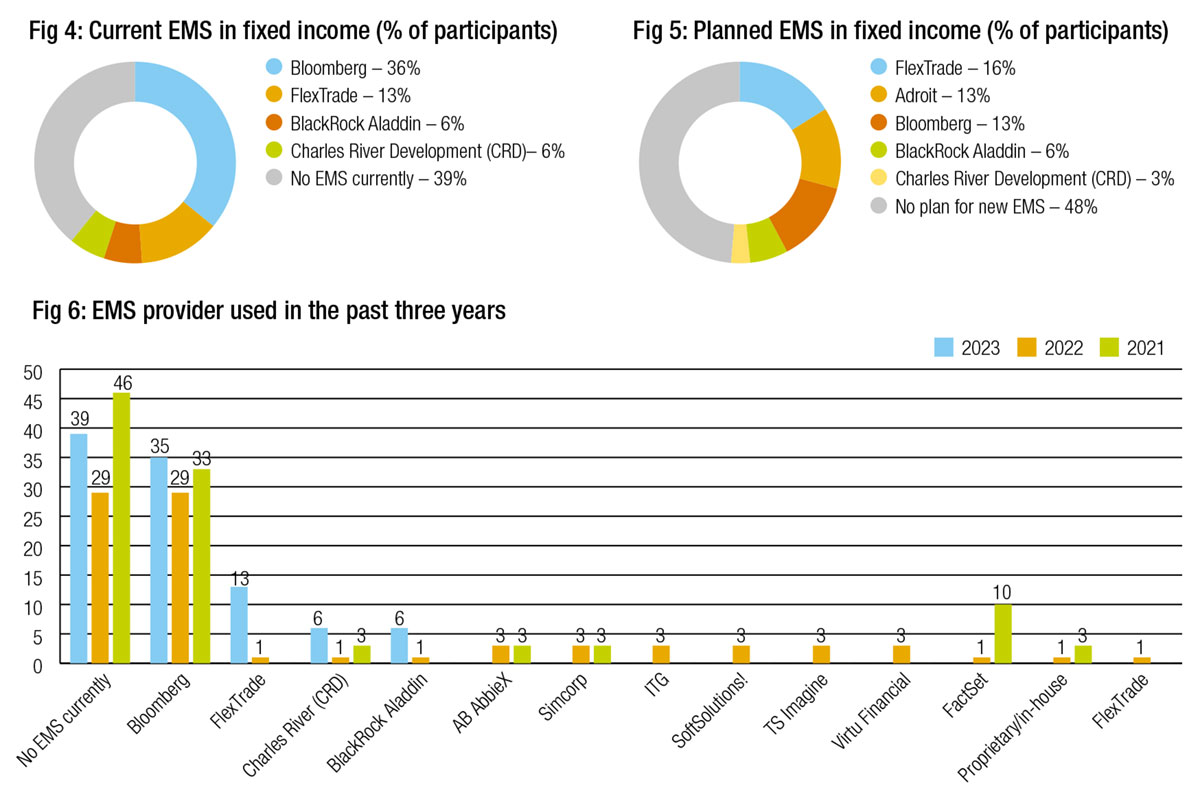

The execution management system (EMS) market has proven more malleable, which is positive news for challengers in the fixed income space such as FlexTrade, TS Imagine and Axe Trading. After two years of showing a strong sales pipeline, FlexTrade is now showing a spike in adoption from buy-side traders, proving itself a resilient proposition despite the headwind that slow onboarding creates (see Fig 4).

It is also clear from examining the last three years that incumbent OMS providers are proving successful in providing EMS functionality, with Aladdin and Charles River featuring more heavily as EMS providers by buy-side respondents (see Fig 6). However, there is clearly a barrier to change which is quite different to that which exists in the OMS space – nearly 40% of firms have no EMS even when counting OMSs stepping into that role. That implies the case for investing in an EMS has not been convincingly made to all buy-side firms.

Nearly half of respondents have no plans to use a new EMS – fewer than are resisting a new OMS – yet several firms including FlexTrade and Adroit who are pure-play EMS providers are showing strong pipelines for new business (see Fig 5).

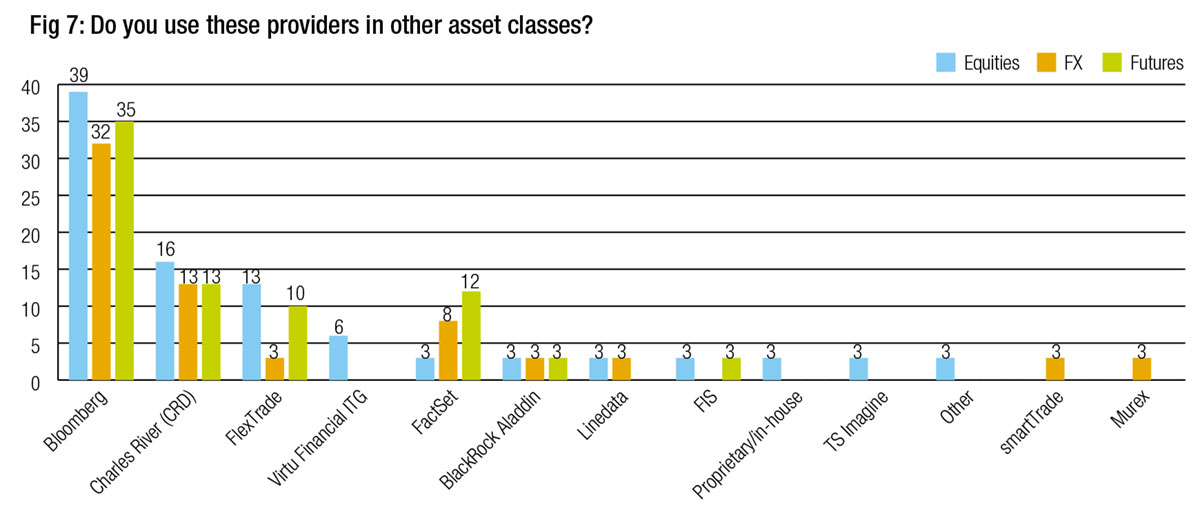

The cross asset space is dominated by Bloomberg, which has the lead in common use across equities, FX and futures, yet many other firms are clearly also getting traction by supporting multi-asset trading, including Charles River, FlexTrade and FactSet (see Fig 7).

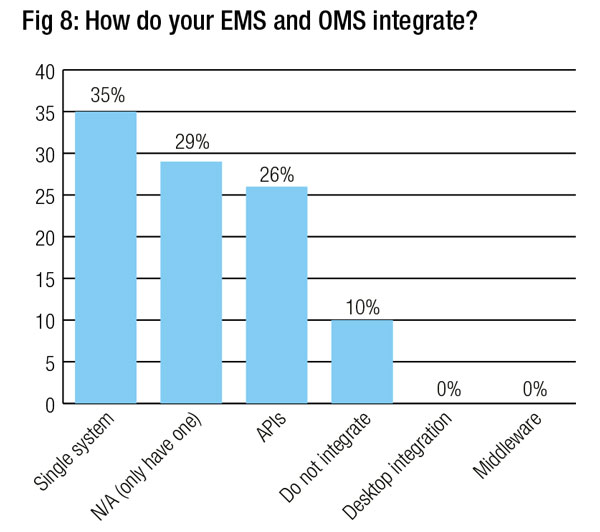

Working across execution and order management systems is a potential barrier to use of EMSs particularly, as any additional operational complexity mitigates the operational advantages that EMS functionality. To that point, we asked how firms were integrating their OMS and EMS systems and found 10% did not have integrated systems and nearly 30% only had one, not both, leaving no need for integration (see Fig 8). Those that did integrate were mainly a single system – 35% – or using APIs to integrate rather than other solutions such as desktop integration software.

Working across execution and order management systems is a potential barrier to use of EMSs particularly, as any additional operational complexity mitigates the operational advantages that EMS functionality. To that point, we asked how firms were integrating their OMS and EMS systems and found 10% did not have integrated systems and nearly 30% only had one, not both, leaving no need for integration (see Fig 8). Those that did integrate were mainly a single system – 35% – or using APIs to integrate rather than other solutions such as desktop integration software.

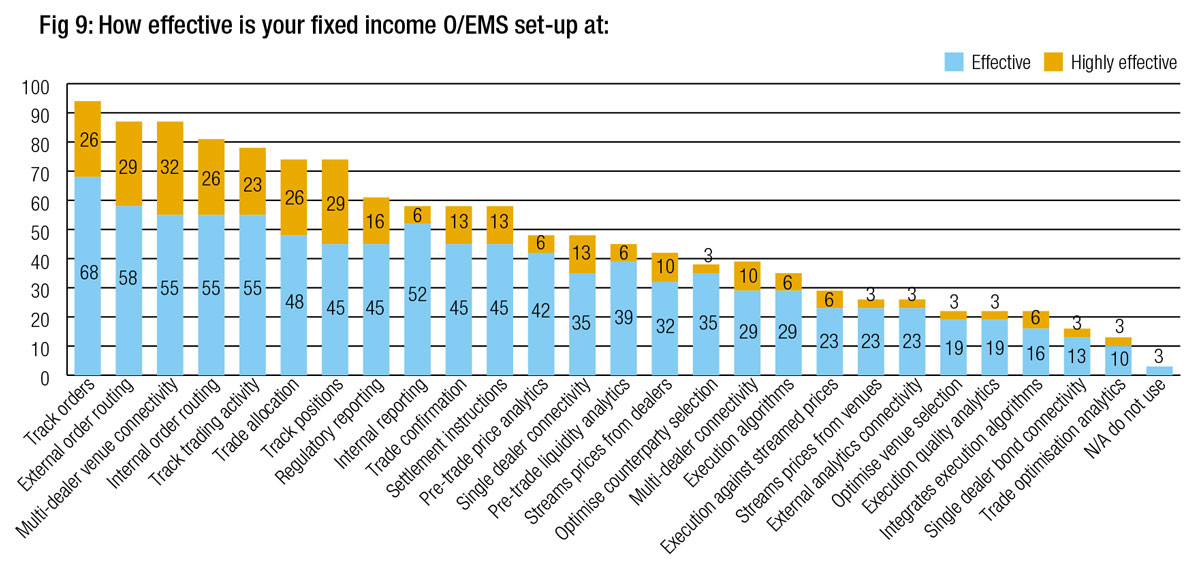

Overall, traders report that their O/EMS set ups are most effective at routing orders both internally and externally, tracking of orders, trade positions and trading activity, as well as supporting trade allocation and connectivity to multi-dealer trading venues (see Fig 9). This is in line with the functionality reported in previous years. We have seen some relatively big changes in function, with tracking of positions, trades and orders all increasing in effectiveness by double figures over the past year, while connectivity to multi-dealer venues also got a boost.

Less than half of all respondents saw pre-trade liquidity and price analytics as effective, and there are still frustrations around the connectivity to dealers and streaming prices directly from them.

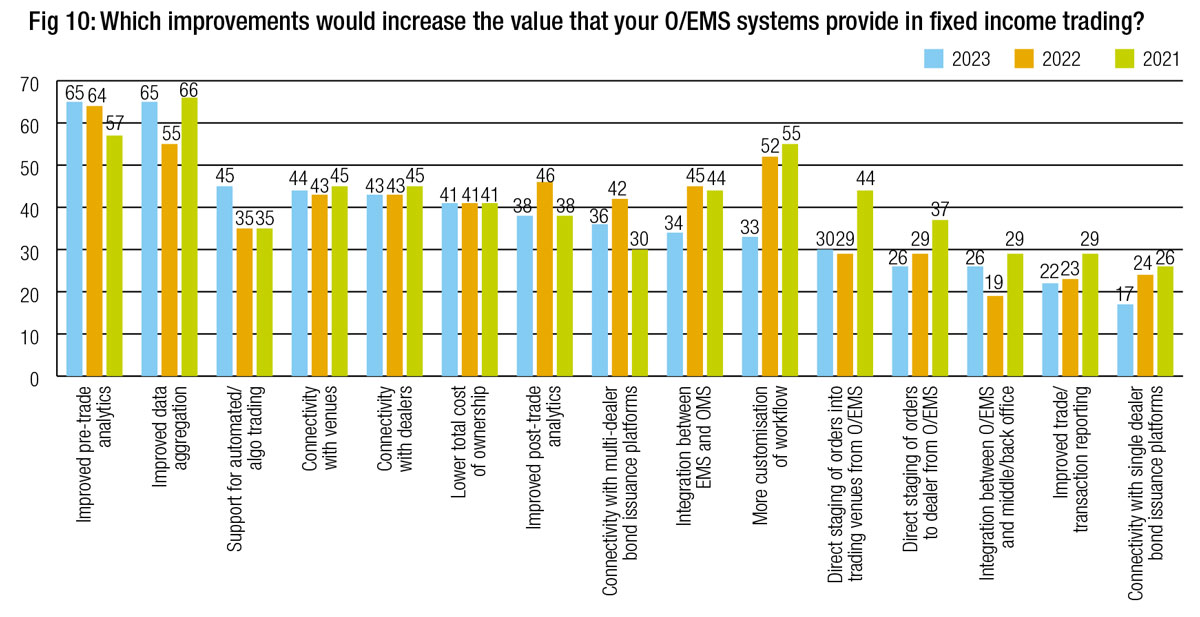

While improved data in fixed income markets is a perennial issue for TCA systems, pre-trade analytics is the main additional service that could deliver improvement to O/EMS functionality followed by improved data aggregation (see Fig 10).

This year we have seen support for algo/automated trading in the O/EMS grow more significantly than any other factor, which fits the more anecdotal discussions heard around the increased desire for automation of fixed income trading.

This study

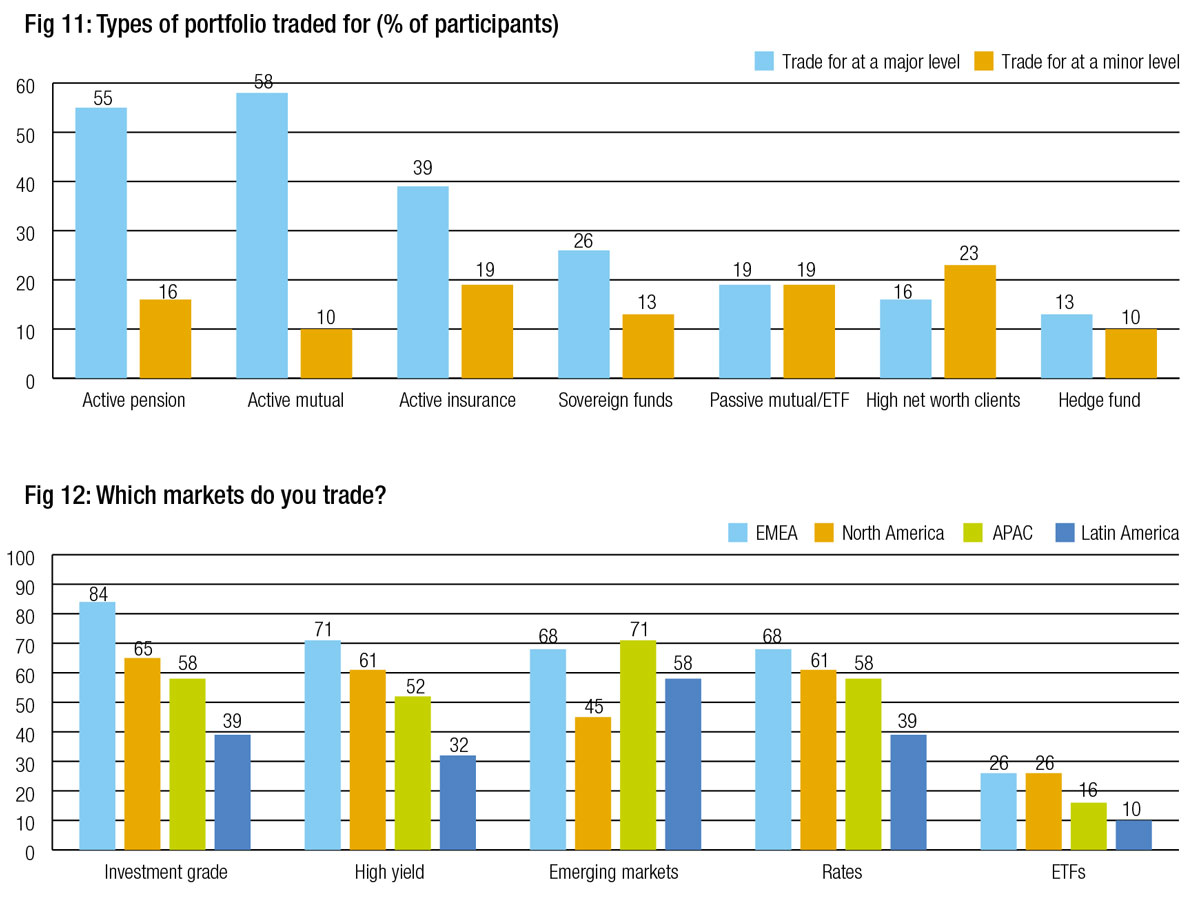

The majority of respondents to this study trade for long only investments either as part of active pension, mutual or insurance funds. A significant proportion also trade for sovereign wealth and passive funds, as for high net worth and hedge funds (see Fig 11). There is a bias toward firms trading investment grade, high yield and rate in Europe, followed by the US (see Fig 12).

©Markets Media Europe 2023

©Markets Media Europe 2025

more valuable")