Sell-side dealers have long benefited from the efficiencies and liquidity that electronic trading brings to the Cash bond and Repo markets. Now, as it celebrates 20 years at the forefront of market innovation, MTS brings the same benefits to the buy-side by combining the functionality, technology and networks of its established D2D Repo and D2C BondVision platforms to create a dedicated new segment on BondVision called Global Collateral Management (GCM).

Whilst other aspects of the fixed income markets have evolved significantly in recent years, Repo trading between dealers and clients (D2C) has remained little changed with the majority of activity still taking place OTC via phone, email and other manual mediums.

With a desktop presence at over 100 sell-side participants on the MTS Repo market, and over 400 buy-side participants on the BondVision Cash Bond market, MTS identified a clear opportunity to leverage this unique position to bring this extended network and two decades of Repo experience together.

Extensive Network

![]() The scarcity of collateral is an increasing issue, particularly following the implementation of new EMIR requirements for OTC derivative margining and continuing ECB market operations. With regulatory pressure on banks’ balance sheets showing no sign of easing, MTS is aware of the need to bring together as many buy- and sell-side participants as possible in order to mobilise cash and collateral to where it is needed most.

The scarcity of collateral is an increasing issue, particularly following the implementation of new EMIR requirements for OTC derivative margining and continuing ECB market operations. With regulatory pressure on banks’ balance sheets showing no sign of easing, MTS is aware of the need to bring together as many buy- and sell-side participants as possible in order to mobilise cash and collateral to where it is needed most.

By technically integrating GCM into its existing interdealer trading technology, MTS gives sell-side dealers immediate access and integration via established connectivity and straight through processing solutions. For the buy-side, a new multi-product front end will enhance the current rates and credit platform with additional Repo and Triparty products for a one stop shop with the potential of automated OMS integration.

Flexible Trading Solutions

Whilst the electronic inter-dealer repo market is dominated by standardised and centrally cleared central limit order books, the D2C markets require a great deal more flexibility and customisation.

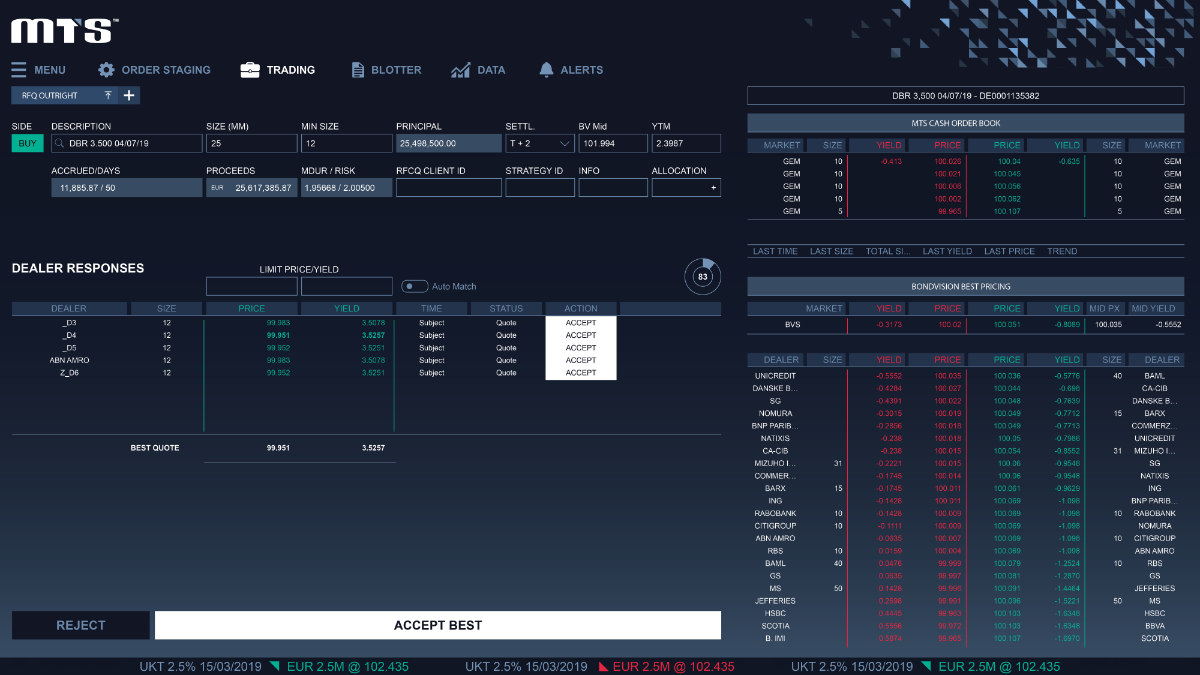

The request for quote (RFQ) trading protocol allows buy-side participants total flexibility over what, when and with whom they trade. From a simple single line RFQ, manually populated and sent to a single dealer, to a List RFQ, automatically imported and sent to a pre-defined group of dealers, the client retains control.

Line by line previews of settlement countervalues, together with the display of “packaged trade” net cash balances enable counterparties to immediately identify the balance sheet impact of potential trades, thus facilitating improved pricing of bonds vs bonds transactions.

Alongside single ISINs and General Collateral baskets, MTS also supports the configuration of bespoke Triparty baskets uniquely defined and mapped to individual counterparties.

At the post trade level, participants have the choice of manual settlement, maintaining full control over settlement instructions, or automated settlement, delegating instruction authority to MTS and further automating full straight-through-processing.

Highly granular credit line controls and configurable haircuts further provide participants with the ability to control their trading activity whilst a full audit trail and best execution records complement the benefits of a regulated trading platform in the eyes of compliance.

Sponsored clearing initiative

As buy-side clients seek to maintain access to banks’ balance sheets, the recently launched Sponsored Clearing Service from LCH has emerged as one viable solution. By offering clients access to the Central Counterparty (CCP) using an agent bank the balance sheet exposure of their counterparties can be significantly mitigated whilst also providing the added security that CCP trading brings.

MTS were quick to see the potential of this model, and have built full support into the GCM market. Whether trading via the RFQ or using the Trade Registration facility to register off venue trades into the CCP, MTS supports fully automated connectivity to this innovative new initiative.

Regulatory changes

With the light at the end of the MiFID II tunnel finally in sight, attention in the repo markets is turning to the new Securities Financing Transaction Regulation (SFTR). Aimed at increasing the transparency of securities financing transactions (SFTs), this wide reaching piece of legislation will require both financial and non-financial market participants to report details of their SFTs to an approved EU trade repository (TR).

With upwards of 100 matching fields needing to be reported by both parties to an SFT, these obligations are leading buy and sell-side participants to look for solutions to ensure easy and accurate dissemination of trade data.

As part of the London Stock Exchange Group (LSEG), MTS will partner with UnaVista, an award winning European Trade Repository to provide a comprehensive solution for participants’ reporting needs.

Technology for today’s market

With the repo market undergoing significant change and with regulatory hurdles both in the present and imminent future MTS’s GCM is uniquely positioned to benefit all users of Repo products with the efficiencies and security that electronic trading brings.

©Markets Media Europe 2025