The DESK profiles five of the major electronic liquidity providers.

Given the strains on market making in fixed income, it is vital that buy-side desks are aware of all available counterparties. Non-traditional market makers have different business models to traditional market-makers, meaning they are not exposed to the same risks, and can be invaluable support. Here we assess the business models and philosophies of major firms.

Jump Liquidity

How do you view ‘liquidity provision’ and ‘market making’ as a firm?

Jump Liquidity was created by Jump Trading, one of the world’s leading market makers, to provide direct access to Jump’s principal liquidity across a variety of global asset classes. Jump draws upon its experience in trading in well over 100 venues worldwide to offer liquidity on a disclosed and customisable basis to its counterparties.

What sets you apart from other ELPs? How do you cover positions?

Jump Liquidity incorporates a wide spectrum of market making approaches with varying holding durations contributing to more diverse liquidity and tighter spreads.

How do you try to support liquidity provision in times of market stress?

Jump provides its counterparties with a consistent trading experience and timely pricing updates throughout challenging market conditions, delivered by best-in-class technology. As a liquidity provider to the markets globally, Jump is committed to being an active market participant during all conditions.

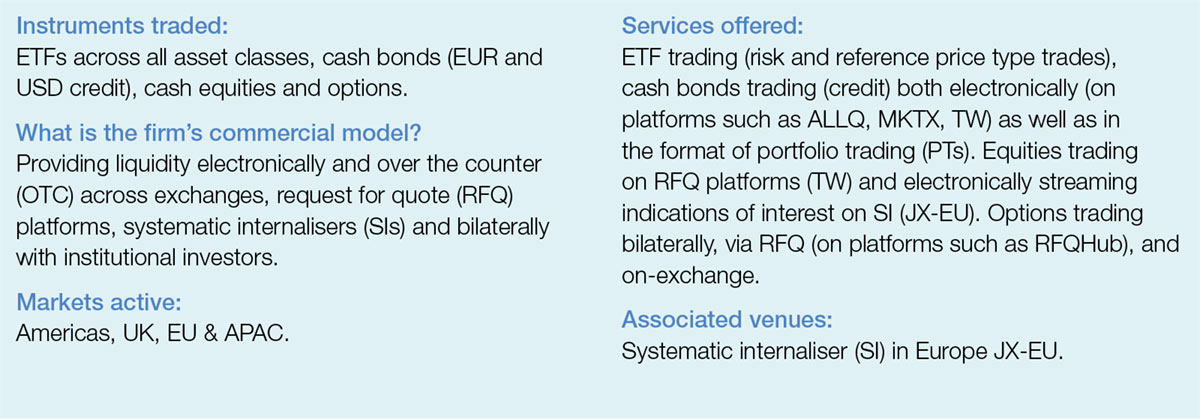

Flow Traders

How do you view ‘liquidity provision’ and ‘market making’ as a firm?

We are a global principal liquidity provider and trading firm, using our capital, sophisticated quantitative analysis and a deep understanding of market mechanics to help keep price consistency at all times.

What sets you apart from other alternative liquidity providers?

We view ourselves as a next generation liquidity provider in fixed income, that leverages technology and innovation as well as automation to enable cost efficient and accurate pricing. Automated pricing results in high response rates, high hit ratios and very fast pricing. Also, our dominant position in ETFs and the increased interaction between the bonds market and the ETF ecosystem gives us an edge that continues to grow on the back of the expected growth of the fixed income ETF AUM (expected to triple over the come years).

How do you cover positions?

We leverage the ETF ecosystem and bond ecosystem in order for them to interact and provide liquidity in both ways. The growing ETF ecosystem adds additional liquidity to the credit markets, since a large amount of bonds are traded by ETF market makers on the back of their Authorised Participant (AP) activities. As ETFs are used as hedging tools for proprietary traders (PTs), and traded without entering the bond market, such as on exchanges, this means liquidity can also enter the bond market in this way. Portfolio trading is a great example where very often the hedge for a portfolio is an ETF or vice versa.

How do you try to support liquidity provision in times of market stress?

Just like our ETF market share, our bond market share continues to grow and continues to provide liquidity and pricing even in volatile times. We support liquidity provision by constantly analysing the dynamics of the market, the large amounts of data allow for us to continuously price in line with market value. Our automated trading strategies allow us to always price very fast.

Jane Street

How do you view ‘liquidity provision’ and ‘market making’ as a firm?

Market making and liquidity provision are the main services we provide to our clients and the market as a whole. By standing ready to buy and sell a broad range of assets at competitive prices, we aim to help support market efficiency and transparency. Additionally, our global presence allows us to provide liquidity 24-hours a day to clients and counterparties around the world.

What sets you apart from other alternative liquidity providers?

Our people and our ability to hold and manage risk. As a result, we excel at handling large and complex trades that are both technologically and operationally difficult. We have a highly collaborative culture and invest heavily in hiring top talent, resulting in largely human-centered trading decisions that are augmented by our high-quality technology and research. We commit our own capital to trading, which allows us to hold positions over longer time horizons than many other ELPs.

How do you cover positions?

Our centralised risk management and robust internal risk systems allow us to maintain a holistic view of the firm’s exposure. Our risk management combined with our broad range of diversified strategies across asset classes and geographies enables us to quickly adapt to new market conditions and trading opportunities.

How do you try to support liquidity provision in times of market stress?

We have a strong track record of remaining active in the market during times of stress, even when many other market participants step away. With a keen eye toward risk, we obsessively model downside scenarios so that if any outlier event happens, we know how to handle it. This preparation, combined with our committed capital, allows us to adapt and continue providing liquidity during periods of market stress.

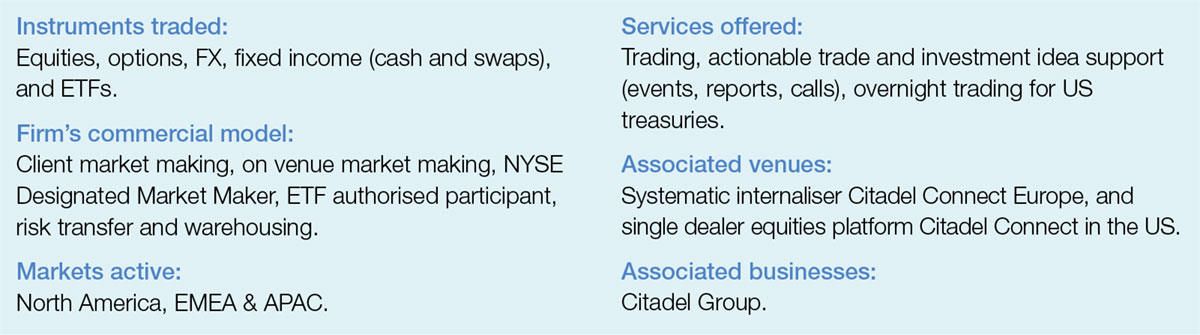

Citadel Securities

Citadel Securities is an electronic market maker, which uses its risk management capabilities and predictive analytics to provide pricing across multiple markets, including during periods of market volatility.

Largely active in the US treasuries market, the model has not been possible to replicate in European government bond markets, partly due to the traditional dealer model which limits competition in the space, according to sources. However, Citadel has voiced interest in this space.

At the European Fixed Income Leaders’ Summit (FILS) in 2022, Will Boeckman, head of E-Sales at Citadel Securities, said, “Liquidity in Gilts right now is much worse than US Treasuries but there is the ability for dealers to toggle the size of how firm they want to be. Is it a value add to the buy side to be streaming £1 million and up firm Gilts? Potentially. Then it is on the dealer to have the technology and risk taking capabilities to be able to adjust with the swings in volatility.”

In 2019, Brian Oliver, then head of Citadel Securities fixed income, currency and commodities unit in Europe, told that year’s FILS, “I think there’s no disagreement that balance sheet constraints have impacted the market over the last four years, regulation has impacted the balance sheet available to the fixed income markets, but I think we should also take comfort that the industry while it continues to work with regulators to get this right, and to optimise that balance between regulatory change and balance sheet and requirements from the dealer community it happens it’s still there’s been quite a bit of innovation.”

As part of Citadel Securities Group (CSG), since 2018 Citadel Securities Europe also provides agency execution, portfolio management, trading algorithm development and support services to affiliates in CSG and has historically taken on staff who had previously been seconded from the wider Citadel Group, as part of a restructuring in the Citadel Securities Group.

In 2022 it formed part of the consortium around RFQ-hub Holdings to support the growth of RFQ-hub, Virtu’s bilateral multi-asset and multi-dealer request-for-quote (RFQ) platform, along with Flow Traders and Jane Street Capital, asset manager BlackRock and electronic trading platform MarketAxess.

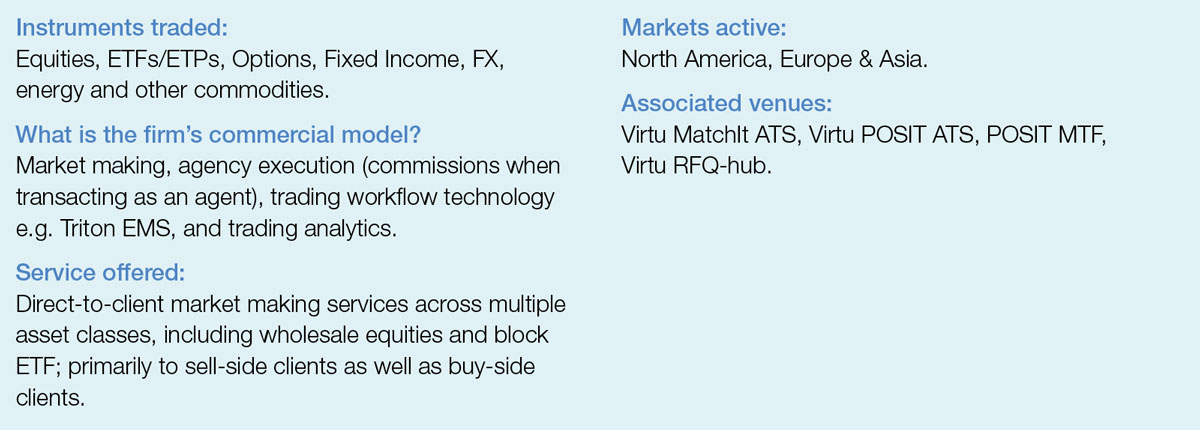

Virtu Financial

The firm has a nascent but growing fixed income capability, having had success in the options space and strong awareness of the importance credit has today, notably for an exchange traded fund (ETF) market maker.

Virtu’s CEO Doug Cifu told analysts in Q4 2021 “We’ve enhanced and began to be a market maker in fixed income. So, we’re expanding the footprint of the firm.”

The firm has a strong history in market making and analytics notably for equities, and has fought hard to break into the fixed income space. Cifu told analysts on an earnings call in Q2 2022 that “It’s still very early in fixed income” but noted the firm has established connectivity to electronic fixed income markets like MarketAxess, Bloomberg and Tradeweb and is onboarding clients.

“We have done our first portfolio trades for clients of corporate credit, which I never thought I would say even as recently as a year ago,” he said. “So I am very proud of the accomplishments we have made there. It’s a big asset class obviously. Historically it has been dominated by dealers who are a number of our competitors that are very meaningful in it. It is important to us because obviously it’s a large asset class.”

Perhaps more importantly he observed, “It is part and parcel of what we offer as a global ETF market maker in order to be in that business. We concluded that we needed to have a corporate credit capability because there’s a lot of fixed income ETF both here, in Europe, and in Asia, so we needed to be in that marketplace and so it was done methodically and strategically. It is not at all the material part of what we do today, but I am optimistic that it will grow in the same way our options capability has grown.”

In May 2022, Virtu Financial formed RFQ-hub Holdings to support the growth of RFQ-hub, Virtu’s bilateral multi-asset and multi-dealer request-for-quote (RFQ) platform. In addition to Virtu, founding consortium members include liquidity providers Citadel Securities, Flow Traders and Jane Street Capital, asset manager BlackRock and electronic trading platform MarketAxess. MarketAxess took a significant minority stake in the platform.

©Markets Media Europe 2025