Concern around liquidity in Europe’s high yield market has been rising over the past quarter as it is hit by a double whammy, falling issuance and declining market making.

The first of these is a response to the rising central bank rates, which are pushing up the cost of borrowing money. For firms with a credit rating that falls into the high yield bracket this cost was typically already high relative to more creditworthy firms – UK’s Metro Bank had to offer a 9.5% coupon in 2019 – and while a pandemic and war have shaken the fundamentals of many businesses, their capacity to borrow has also fallen.

Credit worthiness is certainly one reason some banks are keen to hold less risky debt on their books. Without the ability to rely on debt markets as they had been doing, default rates could rise. Another is the capital cost of holding risky assets. Where banks have an effective model for recycling risk this can be managed more effectively but only a few large US banks fall into that category, according to buy-side traders.

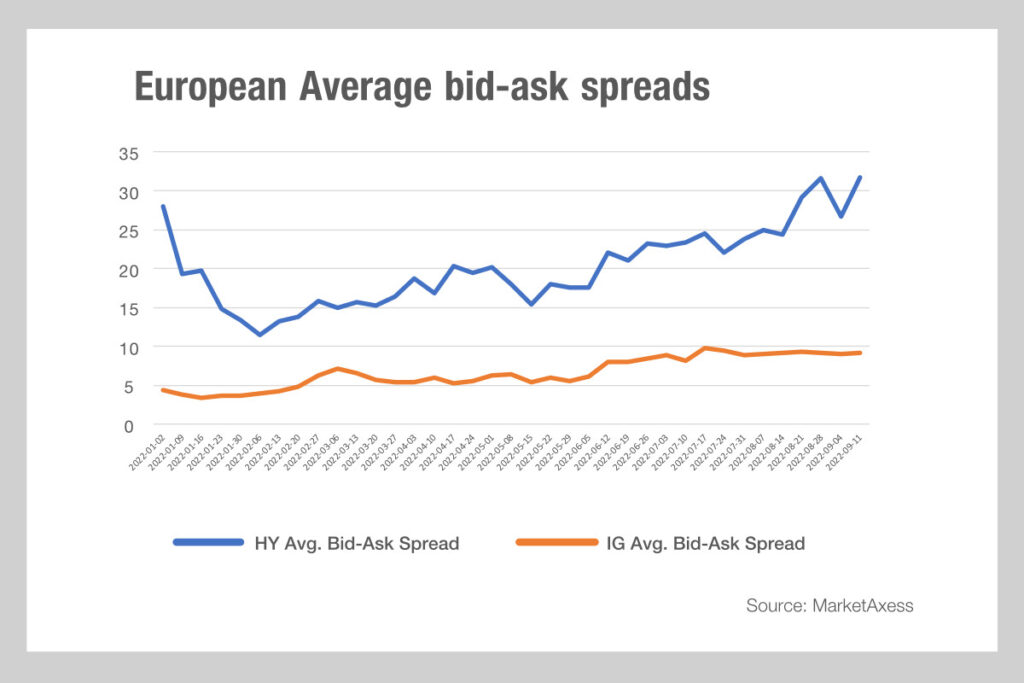

If we look at MarketAxess data, we can see the impact of this on trading costs, via the bid-ask spread. For European HY the mean average has been widening since the start of summer, after contracting somewhat at the end of May. Investment grade (IG) has plateaued over the same period.

We also see this for the median bid-ask spread which at nearly 19 basis points has more than doubled since the start of the year.

Average bid-ask spreads for investment grade trading have doubled over the same period but do not follow the same alarmingly steep path upwards as HY. By contrast the average bid-ask spread for US high yield has fallen since the star of the year, while US IG bid-ask spreads have returned to January levels.

For traders managing activity for high yield funds, this pressure will increase their need to leverage dealer relationships to find the other side of a traded but also to look beyond those relationships where no bids are forthcoming in order to access all-to-all trading, or to consider other ways of expressing the idea into the market, either via other fixed income instruments or trading protocols.

©Markets Media Europe 2025