By Pia Hecher.

Derivatives analytics firm OpenGamma found that transaction costs for derivatives may be misrepresented by up to 900% to investors, as a result of current European rules.

MiFID II and the Packaged Retail and Insurance-based Investment Products (PRIIPs) require asset managers to inform investors about the costs of trading. Asset managers trading instruments including interest rate swaps must consider unpredictable factors driving costs like asset maturity, volatility and the widening or tightening of spreads. But calculating costs is extremely difficult because prices of illiquid derivatives are not observable in the market.

“The underlying issue is that too many asset managers continue to follow the broad nature of the MiFID II rules, applying a ‘one-size fits all approach’ for non-standardised derivatives, which only leads to inaccurate results. Without prescriptive details within the regulation, it is very easy to overestimate,” said OpenGamma CEO Peter Rippon.

Mispricing causes investors to make uninformed decisions on how to allocate money between firms, and investors may even withdraw their money, says Veeral Manek, quantitative analyst at OpenGamma.

“For the asset managers and their traders, this translates to a loss in business in addition to the potential regulatory breach of delivering inaccurate reports,” Manek explains.

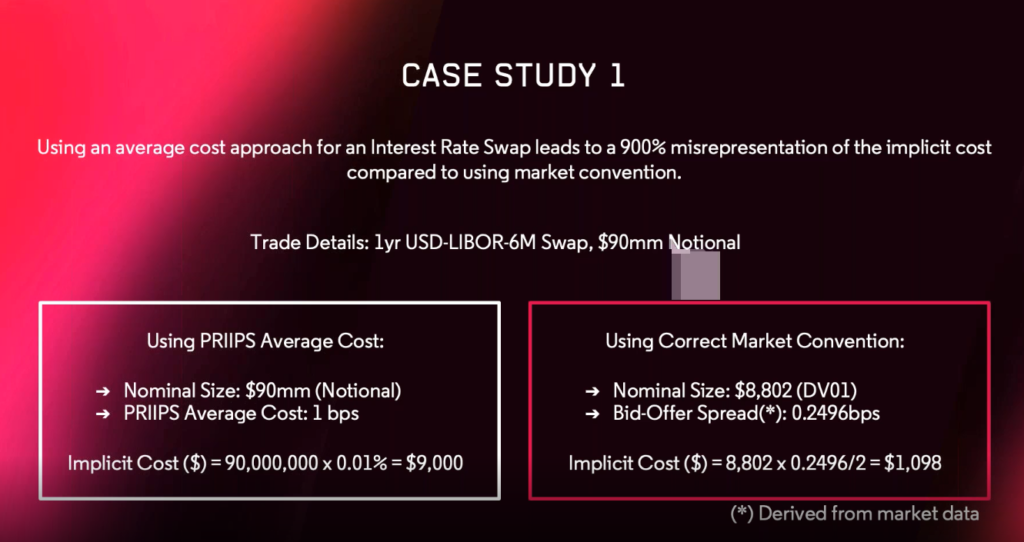

In one example (see pic 1), the firm found that evaluating an interest rate swap using the PRIIPS method vs market convention could lead to an overestimation of cost by 900%.

Pic 1

“When we demonstrate the impact on the cost estimates of using a broad estimation approach versus using one that takes into account all the variables that drive the bid-offer spread of each trade [to asset managers], there is usually a recognition that the broad estimation approach produces inaccurate results. They also acknowledge that, without internal expertise, it is a complex problem to solve,” Manek adds.

As a precaution, Manek advises investors to scrutinise numbers they receive from asset managers in more detail. However, since many investors may not be able to fully understand the impacts of misrepresentation, Manek argues asset managers must ensure an accurate representation of numbers to investors.

Mispricing affects fixed income investors worse than other investors, as fixed income derivatives are commonly used for hedging, so that asset managers trade them in high volumes, Manek states. “Derivatives are the primary cause for cost misrepresentation as the illiquidity and lack of market data make it very difficult to accurately estimate costs without sophisticated financial modelling.”

©TheDESK 2019

©Markets Media Europe 2025