Institutional investors are clamouring for cash as they exercise caution around equities and fixed income over wider macroeconomic uncertainties, according to State Street Holdings Indicators. The near 1% rise in allocations to cash was the largest in ten months and came at the equal expense of equities and bond holdings, the firm said.

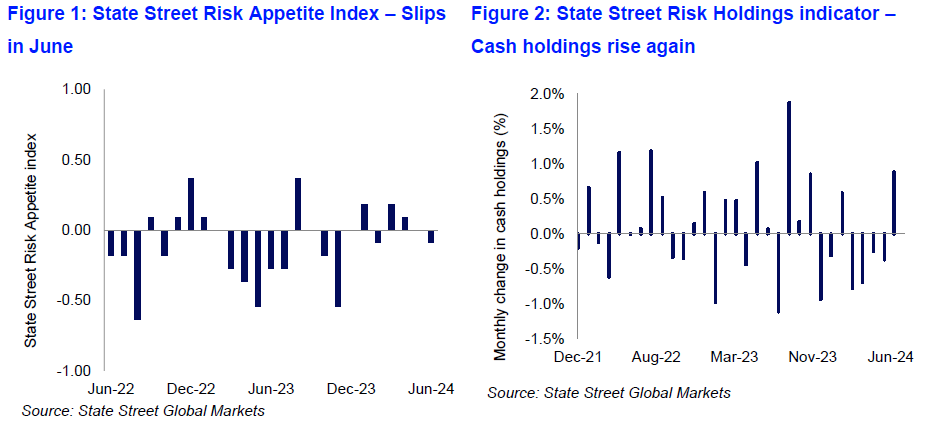

The State Street Holdings Indicators showed that long-term investor allocations to equities fell 42bps to 53.2%. Allocations to fixed income also fell a similar amount (46bps) to 27.5%, which meant cash holdings rose 88bps to 19.3%. This marked the largest rise in cash holdings since last August (Figure 2), while the State Street Risk Appetite Index fell back to -0.09 in June (Figure 1), reflecting a modest risk off bias across the month.

Michael Metcalfe, head of macro strategy at State Street Global Markets, said, “Equity markets may have made new highs, but long-term investors are getting more cautious. After the recent moderate improvement in risk appetites in Q2, institutional investors rushed back to cash in June as a combination of positioning, political risk and cyclical doubts challenged views in both equity and bond markets.”

Metcalfe added: “Investor optimism toward Chinese equities faded in June with flows falling back from above to simply average levels. This did not deter stronger long-term investor inflows into other regional markets such as Korea, India and Indonesia, but it shows that investor sentiment toward Chinese equities remains somewhat fragile even after a better start to the year.

“In Japan the strongest pace of JPY selling in three years abated in June as long-term investors hesitated to add to their building underweight in the currency in the face of increased risks of FX intervention or the growing possibility of imminent policy action from the Bank of Japan in the face of the increasingly uncontrolled weakness in the currency.

“The US will face its own political event risk later this year, but the lesson from June was that the US dollar remains investors’ safe haven of choice in the face of event risk. Long-term investor demand for the USD rebounded smartly in June, alongside demand for the utilities sector in equities and cash more generally.

“Just a month ago we speculated whether long-term investors would tolerate their cash holdings falling below their long-term average given ongoing event risk. June provided a definitive answer to this,” noted Metcalfe.

The Institutional Investor Indicators are designed to measure investor confidence or risk appetite quantitatively by analysing the buying and selling patterns of institutional investors derived from State Street’s US$43.9 trillion in assets under custody and administration. The Risk Appetite Index is derived from measuring investor flows in twenty-two different dimensions of risk across equities, FX, fixed income, commodity-linked assets, and asset allocation trends. The index captures the proportion of the twenty-two risk elements that saw either risk seeking or risk reducing behaviour.

©Markets Media Europe 2024

©Markets Media Europe 2025